Workers’ compensation insurance is a commercial insurance policy that covers medical expenses, wage replacement, and rehabilitation when employees are injured during work activities. For retail businesses, insurance premiums are generally calculated using payroll, job classification codes, claims history, and state regulations.

Retail stores such as clothing boutiques, grocery stores, hardware retailers, and convenience stores usually have moderate workers’ compensation risk levels. Because retail work typically involves customer service, stocking merchandise, and operating registers, the injury risk is lower than industries such as construction or manufacturing. However, retail employees still face workplace hazards such as lifting inventory, stocking shelves, and assisting customers.

Key Takeaways

- Retail workers’ compensation insurance usually costs $0.40 to $2.00 per $100 of payroll.

- Small retail businesses often pay around $80 to $100 per month, or about $1,000 per year.

- Insurance premiums are calculated using payroll, classification codes, and experience modification factors.

- Claims history, employee job risk, and state regulations can increase or decrease workers’ compensation costs.

- Retail businesses can lower premiums by improving workplace safety and employee training.

Average Workers’ Compensation Insurance Cost for Retail Businesses

Retail business owners frequently ask the question. What is the average workers’ compensation insurance cost for retail businesses?

Workers’ compensation premiums for retail businesses typically range between $0.75 and $2.00 per $100 of payroll. The exact premium depends on payroll size, employee job roles, risk classification codes, and previous claims history.

Insurance carriers use payroll as the primary exposure measurement. A higher payroll indicates more employee work hours and therefore a higher probability of workplace injury claims.

Example premium ranges for retail businesses are shown below.

| Annual Payroll | Rate per $100 Payroll | Estimated Annual Premium |

| $100,000 | $1.00 | $1,000 |

| $200,000 | $1.25 | $2,500 |

| $400,000 | $1.50 | $6,000 |

Retail businesses with larger staff sizes or higher employee wages generally pay higher workers’ compensation premiums because the payroll exposure increases.

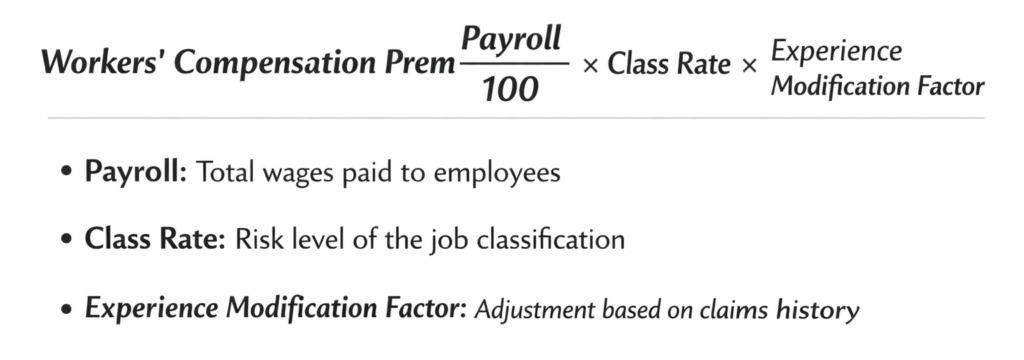

How Workers’ Compensation Insurance Costs Are Calculated

Insurance carriers use a standardized premium calculation formula that includes payroll, classification rates, and risk adjustment factors.

The mathematical formula used to estimate workers’ compensation premiums is:

Where

- Payroll represents the total wages paid to employees

- Class Rate represents the risk level of the job classification

- Experience Modification Factor represents past claims performance

Insurance companies evaluate several attributes when calculating workers’ compensation premiums.

Payroll Size and Employee Wages

Payroll represents the total wages paid to employees during a policy period. Because workplace injuries occur during employee work activities, payroll is used to estimate exposure to workplace accidents.

Retail businesses with larger payroll totals typically pay higher workers’ compensation premiums.

Example payroll impact.

| Payroll | Class Rate | Estimated Premium |

| $150,000 | $1.10 | $1,650 |

| $300,000 | $1.10 | $3,300 |

Higher payroll means more employee work hours, which increases the probability of injury claims.

Retail Industry Classification Codes

Another important factor in premium calculation is workers’ compensation classification codes.

Classification codes identify the type of work employees perform. Insurance companies assign risk levels to these job categories.

Retail businesses are commonly classified under NCCI retail classification codes.

| Class Code | Description |

| 5403 | Carpentry NOC |

| 5551 | Roofing |

| 8810 | Clerical Office Employees |

Employees who perform stockroom lifting tasks or warehouse duties may have higher risk ratings than cashiers or sales associates.

Number of Employees

The number of employees directly affects payroll totals. Businesses with larger teams generate higher payroll exposure and therefore higher workers’ compensation premiums.

Retail stores often hire:

- full time employees

- part time employees

- seasonal holiday staff

All eligible employees must be included in payroll calculations for workers’ compensation coverage.

Claims History and Risk Profile

Insurance carriers analyze a company’s claims history when determining premium rates.

Businesses with frequent workplace injury claims may receive higher premiums because they present a higher risk profile.

Conversely, retail businesses that maintain strong workplace safety programs and low injury rates may receive discounted workers’ compensation premiums.

Claims severity also matters as a single minor claim may have minimal effect, while repeated injury claims may significantly increase insurance costs.

Experience Modification Factor (E-Mod)

The experience modification factor, often called E Mod, adjusts premiums based on a business’s previous claims performance.

| Experience Modifier | Meaning |

| 0.85 | Lower risk than average |

| 1.00 | Industry average risk |

| 1.25 | Higher than average risk |

An E Mod lower than 1.00 may reduce workers’ compensation premiums. An E Mod higher than 1.00 may increase insurance costs.

State Workers’ Compensation Regulations

Workers’ compensation insurance rules are regulated by individual states. Each state determines:

- employer coverage requirements

- premium rate structures

- compliance regulations

Because of these differences, workers’ compensation insurance costs vary across states.

Workers’ Compensation Insurance Cost by Type of Retail Business

Retail businesses vary in their workplace environments and employee tasks. These differences affect workers’ compensation insurance costs.

Clothing Stores

Clothing stores generally experience lower workers’ compensation rates. Employees mainly assist customers, organize merchandise, and operate registers. However, risks still exist from ladder use, inventory stocking, and repetitive motion tasks.

Convenience Stores

Convenience stores often operate extended hours and receive frequent inventory deliveries. Employees stock shelves, manage refrigerated inventory, and interact with customers regularly. These activities slightly increase workplace injury risk.

Grocery Stores

Grocery stores often have higher injury exposure compared to small retail stores. Employees handle heavy boxes, stock shelves, and work in refrigerated areas. Lifting injuries and slip hazards are common.

Hardware Stores

Hardware stores sell heavy equipment, tools, and construction materials. Employees frequently lift bulky merchandise and assist customers with large purchases. These activities increase lifting injury risk.

Specialty Retail Shops

Specialty retailers such as electronics stores or jewelry stores generally experience moderate risk levels. Employee tasks include customer assistance, product demonstrations, and inventory management.

Workers’ Compensation Insurance Costs in California

Workers’ compensation insurance for retail businesses in California typically ranges from $0.40 to $1.00 per $100 of payroll, depending on employee job duties, claims history, and insurance carrier underwriting policies.

For many small retail businesses, this cost translates to approximately $80 to $100 per month, or around $1,000 to $1,200 per year. Some very small retail shops with limited payroll and low risk job roles may find policies starting as low as $15 to $20 per month, while larger retail operations may pay significantly higher premiums.

Example cost estimates for retail businesses in California are shown below.

| Annual Payroll | Estimated Rate per $100 Payroll | Estimated Annual Premium |

| $100,000 | $0.40 | $400 |

| $200,000 | $0.75 | $1,500 |

| $300,000 | $1.00 | $3,000 |

California requires employers with one or more employees to maintain workers’ compensation insurance coverage. Retail businesses that fail to carry workers’ compensation insurance may face legal penalties, fines, and full financial responsibility for employee medical expenses and lost wages after workplace injuries.

Insurance premiums in California are influenced by several attributes:

- payroll totals

- retail classification codes

- employee injury risk

- claims history

- experience modification rating

Retail businesses that maintain strong safety programs and low injury rates may qualify for lower workers’ compensation insurance premiums over time.

Common Workplace Injuries in Retail Businesses

Retail stores may appear low risk, yet employee injuries occur regularly due to daily operational tasks.

Slips and Falls

Slips and falls are among the most common retail workplace injuries. Wet floors, spilled products, and tracked rainwater can create hazardous walking surfaces.

Stockroom and Lifting Injuries

Retail employees frequently lift merchandise, move boxes, and restock shelves. Improper lifting techniques can lead to back strains and muscle injuries.

Repetitive Motion Injuries

Repetitive tasks such as scanning products, folding clothing, and stocking shelves can lead to repetitive strain injuries affecting wrists, elbows, and shoulders.

Customer-Related Incidents

Retail employees interact with customers throughout the day. Occasionally employees may be injured while assisting customers or handling disturbances in the store.

How Retail Businesses Can Lower Workers’ Compensation Insurance Costs

Several operational strategies can help reduce workplace injury risk and improve insurance rates.

Implement Workplace Safety Programs

Retail businesses can introduce workplace safety programs that include slip prevention procedures, ladder safety guidelines, and safe inventory handling practices.

Provide Employee Training

Employee training helps workers recognize hazards and follow safe work procedures. Proper lifting techniques and equipment handling training can significantly reduce workplace injuries.

Maintain Accurate Job Classifications

Employers should ensure employees are assigned to the correct workers’ compensation classification codes. Incorrect classification may result in inaccurate premium calculations.

Create Return-to-Work Programs

Return to work programs allow injured employees to perform modified duties during recovery. This approach helps reduce claim costs and shorten disability periods.

Bundle Commercial Insurance Policies

Retail businesses may reduce insurance costs by bundling workers’ compensation coverage with other commercial insurance policies such as general liability insurance or property insurance.

How to Choose the Right Workers’ Compensation Coverage for a Retail Business

Retail businesses should carefully evaluate their workers’ compensation coverage needs.

Business owners should consider:

- payroll totals

- employee job duties

- state regulatory requirements

- workplace risk exposure

Independent insurance agents can compare insurance carriers and help retail businesses select policies that provide appropriate coverage.

Frequently Asked Questions About Workers’ Compensation Insurance Costs

Do part-time retail employees require workers’ compensation coverage?

Yes. In most states part time employees must be covered under workers’ compensation insurance if they are classified as eligible employees.

Does workers’ compensation cover customer-related injuries to employees?

Yes. Workers’ compensation insurance covers employee injuries that occur during job duties, including incidents that happen while assisting customers, managing disputes, or handling store operations.

Can a retail business owner be excluded from workers’ compensation coverage?

In some states, business owners, partners, or corporate officers may choose to exclude themselves from workers’ compensation coverage. However, eligibility rules vary by state and insurance regulations.

Get a Workers’ Compensation Insurance Quote for Your Retail Business

Retail business owners benefit from reviewing their workers’ compensation coverage regularly. An experienced insurance advisor can evaluate payroll, employee roles, and workplace risks to estimate insurance premiums.

First State Insurance works with businesses across multiple industries and helps retail companies obtain workers’ compensation policies tailored to their operational risks and regulatory requirements. Retail business owners who want an accurate estimate of workers’ compensation insurance cost can request a personalized quote and policy review from an experienced insurance professional.